Money

Money management isn’t about restriction—it’s about control and intention. When you shift your mindset, budgeting becomes a tool for freedom, helping you spend on what truly matters while avoiding unnecessary stress. With a clear system in place, you stop guessing where your money goes and start making confident, purposeful financial decisions.

Part 1: Shift Your Mindset — Budgeting = Freedom, Not Limitation

Most people think budgeting means saying “no” all the time.

In reality, it means:

- Saying yes to what matters most

- Spending intentionally instead of impulsively

- Removing financial stress and uncertainty

When every dollar has a purpose, you can enjoy your money without guilt—because your priorities are already covered.

Part 2: Know Where Your Money Goes (The 30-Day Audit)

You can’t fix what you don’t measure.

Action Step: Track Every Expense for 30 Days

- Record all spending (manual or via app)

- Categorize expenses

- Identify patterns and leaks

At the end of the month, you’ll clearly see:

- Where your money is actually going

- Which expenses are unnecessary

- Where adjustments are possible

Key insight: Awareness is the foundation of financial control.

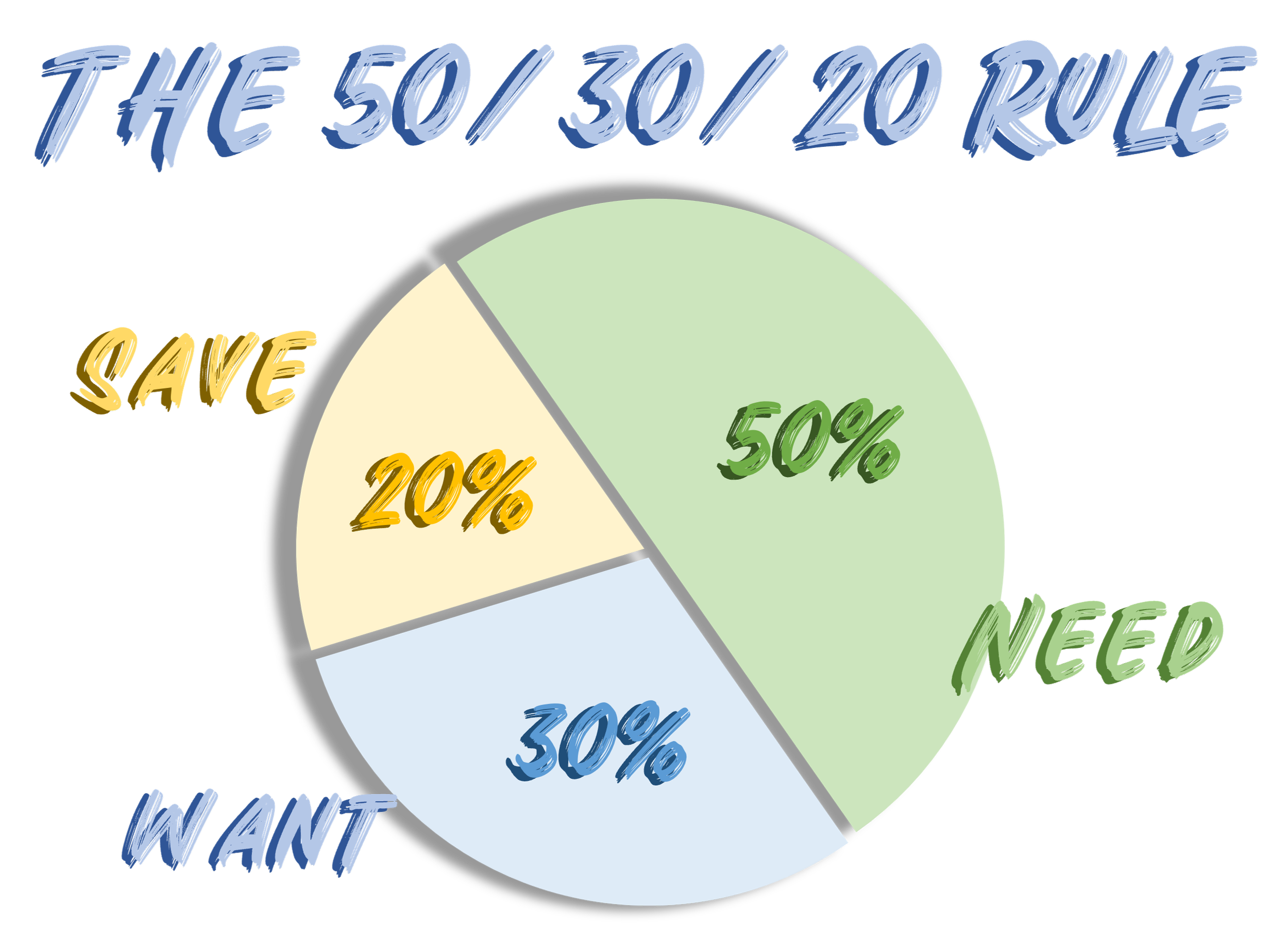

Part 3: Use the 50/30/20 Rule (Simple & Effective Framework)

This rule divides your after-tax income into three categories:

1. 50% for Needs (Essential Expenses)

These are non-negotiables:

- Rent or mortgage

- Groceries (basic)

- Utilities

- Transportation

- Insurance

- Minimum debt payments

If this exceeds 50%, your cost of living may be too high relative to your income.

2. 30% for Wants (Lifestyle Spending)

This is your “enjoy life” budget:

- Dining out

- Shopping

- Entertainment

- Travel

- Subscriptions

Why it matters: This category prevents burnout and makes budgeting sustainable.

3. 20% for Savings & Debt Repayment

This is where real financial growth happens.

Priority order:

- Build emergency fund ($500–$1,000)

- Pay off high-interest debt

- Invest for long-term goals

Part 4: Make It Work in Real Life

1. Pay Yourself First

Before spending anything:

- Automatically transfer money to savings

- Treat savings like a fixed expense

Result: Saving becomes automatic, not optional.

2. Set Spending Limits

Define clear budgets for categories like:

- Food

- Entertainment

- Shopping

Monitor spending weekly to avoid overshooting.

3. Spend Without Guilt

Once your plan is set:

- Enjoy your “wants” category fully

- Stop feeling guilty about spending

This is the goal of a balanced budget.

Part 5: What If Your Budget Doesn’t Work?

If your numbers don’t add up, adjust strategically:

Step 1: Reduce “Wants” First

- Cancel unused subscriptions

- Eat out less frequently

- Replace habits with cheaper alternatives

Step 2: Optimize “Needs”

- Negotiate bills

- Switch service providers

- Reduce fixed costs where possible

Step 3: Increase Income

- Side hustles

- Freelance work

- Sell unused items

Reality: You can only cut so much—but income has no fixed ceiling.